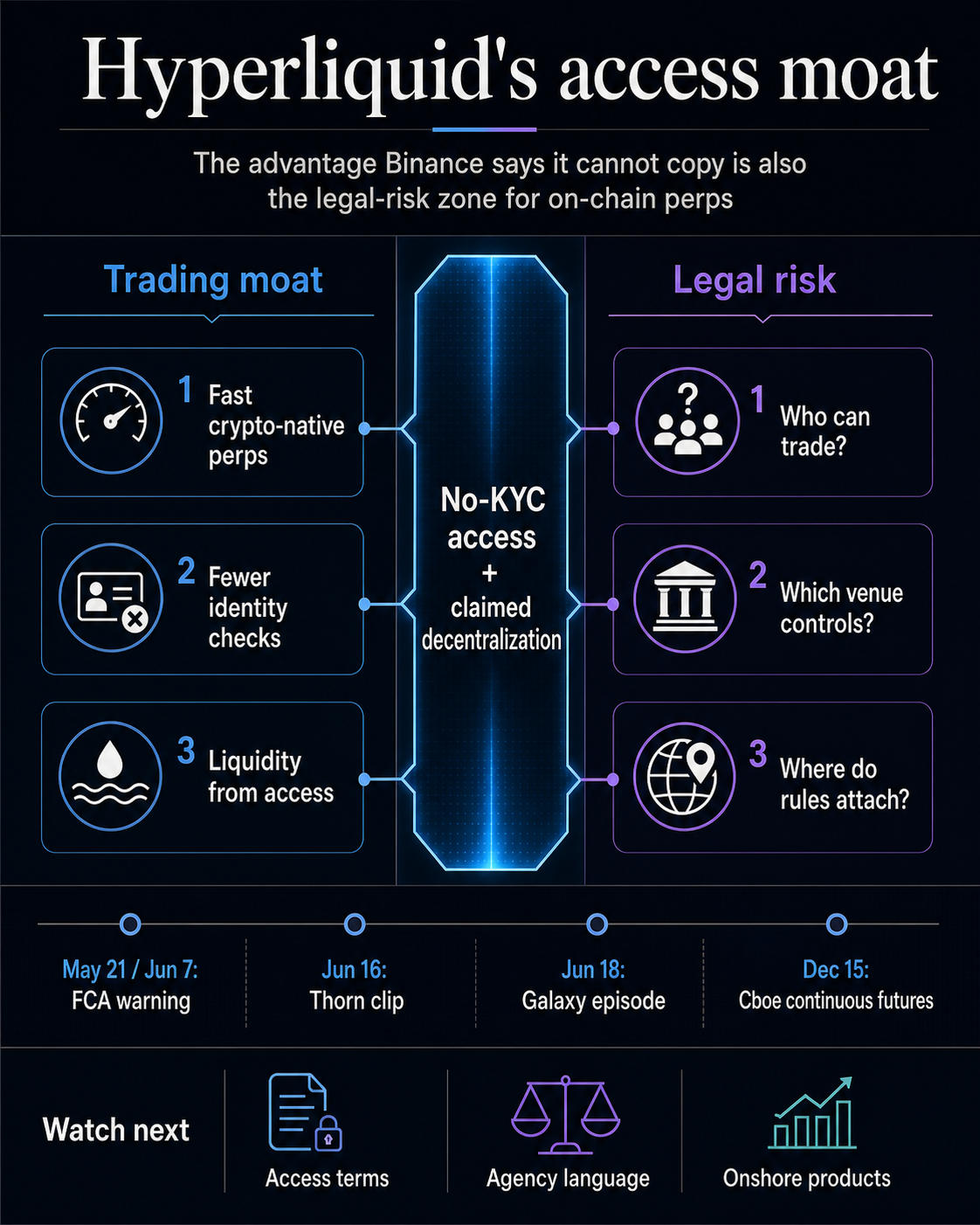

Hyperliquid’s biggest advantage is starting to look like its cleanest legal risk: the no-KYC access model CZ says Binance cannot copy.

In a Galaxy Brains episode published June 18, Galaxy’s Alex Thorn spoke with Binance founder Changpeng Zhao about the crypto cycle, perps moving onshore, prediction markets, and Hyperliquid’s no-KYC model.

Thorn’s June 16 clip made the distinction clear: CZ praised Hyperliquid’s product, said Binance cannot compete with a niche built around no KYC and claimed decentralization, and said he would not run that model given his own experience.

The discussion has also evolved beyond CZ simply saying Binance cannot compete in Hyperliquid’s niche. Subsequent chatter focused on his saying Hyperliquid’s model was “awesome,” but also noted that he assumed the project had “good lawyers.” That remark exposed the regulatory dimension of the debate by tying the platform’s competitive edge directly to legal and compliance risk.

That distinction turns a product compliment into a market-structure problem. One derivatives platform now faces a broader conflict over which parts of on-chain perps-regulated exchanges can copy.

Hyperliquid’s moat includes more than faster trading, crypto-native design, or trader loyalty. It is the ability to offer perpetual futures-like markets with an access model that feels different from a centralized exchange operating under the compliance expectations now attached to major global venues.

If on-chain perps keep growing because they feel open, fast, and less intermediated, the policy conflict becomes whether that same openness can survive scrutiny of who is being served, what products are being offered, and who is responsible when a venue claims decentralization.

The access advantage CZ pointed to

CZ’s answer carries weight because Binance is the exchange most associated with global crypto derivatives scale, and because he separated product admiration from operating risk. Hyperliquid can be good at what it does while running in a lane Binance does not want to enter.

That distinction is the core of the market-structure fight. Regulated venues can improve matching engines, extend trading hours, list more crypto-linked contracts, and design products that more closely resemble perpetual exposure.

The harder part to reproduce is the user experience of trading without the same identity checks, jurisdictional filters, or centralized compliance gates that come with regulated exchange status.

Hyperliquid’s own terms and onboarding documentation are therefore part of the operating risk. The exact wording around access, eligible users, restricted jurisdictions, and user obligations is where the trading model becomes a policy object.

A product can be technically decentralized in some ways and still draw scrutiny over who operates the interface, who promotes access, and how users from restricted markets are kept out.

The clearest implication of CZ’s remarks is that Hyperliquid is competing from a different risk position. Binance can compete on liquidity, listings, brand, and infrastructure.

It is much harder for Binance to compete by giving up the compliance posture that now defines its global operating model.

The practical consequence is simple. If no-KYC access is what traders value most, then the market leader in that lane may be the venue most exposed to the question of whether the model can keep scaling without becoming more like the exchanges it disrupted.

The access model also reaches beyond derivatives specialists. The trading edge sits in a user promise: fewer barriers between a trader and a leveraged market.

That promise can drive liquidity, but it also gives regulators a concrete place to examine who controls the market and which users are being reached.

Why the legal risk is already visible

The legal risk is concrete but bounded. CZ was offering his own view, not a regulatory finding, and the concrete official marker is a UK warning rather than a US action.

The UK’s Financial Conduct Authority has published a warning page for Hyperliquid, first posted on May 21 and updated on June 7, saying the firm may be providing or promoting financial services without permission and may be targeting people in the UK.

As of press time, the warning remains active and continues to frame Hyperliquid as an unauthorized firm that may be targeting UK users. It has become one of the clearest public examples of regulators treating a major on-chain perpetuals venue as more of a financial-services provider than a neutral software infrastructure.

That warning already put Hyperliquid’s Wall Street ambitions under a regulatory lens, while CZ’s remarks add a different concern. Regulators may also ask whether the same no-KYC posture that makes the platform hard to match also makes it hard to normalize.

US history gives that risk sharper edges without making Hyperliquid the target of the same facts. In 2022, the CFTC brought its action against bZeroX and Ooki DAO, alleging illegal off-exchange digital-asset trading, registration failures, and Bank Secrecy Act violations tied to leveraged and margined retail commodity transactions.

The action carries a limited lesson: US derivatives regulators have previously argued that decentralized or DAO-linked structures can still fall within regulatory reach.

That precedent leaves Hyperliquid outside the facts of the case while showing why officials may focus on access. If a venue offers products that behave like derivatives and reaches users regulators believe should be protected or screened, the debate can shift from code and community to promotion, venue control, and accountability.

Decentralization claims carry a double edge. The more credibly a platform can demonstrate that it operates outside the conventional intermediary model, the stronger its argument against being treated as one.

The more users experience it through identifiable front ends, promotional channels, market incentives, and practical controls, the easier it becomes for regulators to ask who is actually responsible for the market.

For traders, decentralization becomes practical rather than rhetorical. The more a venue relies on visible interfaces, incentives, and user flows, the more officials can focus on the parts of the system that still appear to be governed by people, policies, and market design choices.

Onshore products change the comparison

The other half of the competitive risk is regulated market design. Galaxy’s episode description placed CZ’s Hyperliquid remarks alongside perps coming onshore at CME and CBOE.

The product gap between offshore crypto-native venues and regulated markets is not static.

Cboe announced in November 2025 that its futures exchange offering continuous futures for Bitcoin and Ether.

The exchange’s Bitcoin and Ether Continuous Futures are trading as U.S.-regulated products designed to provide perpetual-style exposure through long-dated contracts with daily funding adjustments.

The policy fight over crypto perpetual futures regulation and related venue-classification disputes has also intensified as prediction markets and perps-like products press against older market categories.

The comparison still depends on product design and legal status. Regulated continuous futures differ from Hyperliquid-style on-chain perps in custody, margining, venue control, access, and the operator’s legal status.

But the more regulated venues bring continuous crypto exposure onshore, the more competition shifts. Hyperliquid’s defense has to rest on the whole package, including access, on-chain settlement, and market culture, remaining meaningfully different.

CZ’s remarks land there. If regulated exchanges can close part of the product gap while preserving KYC and venue oversight, Hyperliquid’s advantage becomes more concentrated in the part regulated players least want to copy.

That is good for differentiation until it becomes the exact part regulators treat as unacceptable.

The policy fight around prediction markets adds another layer. As perps-like exposure, event contracts, and continuous futures move closer to regulated venues, agencies and courts will have more chances to define which products belong under which rules.

That makes the distinction between product shape and access model more important. Hyperliquid can win traders with a different experience, but that experience is exactly what makes future official language important.

A regulated venue can reduce the product gap without changing the access gap. That distinction is the reason CZ’s remarks cut through ordinary exchange rivalry.

If onshore markets keep improving, the remaining advantage shifts toward the feature that carries the most policy pressure: who can trade, from where, and under which checks.

Access changes would define the moat

Hyperliquid’s own public language now carries more weight: terms, onboarding, jurisdiction blocks, front-end controls, and any shift in how the platform describes user eligibility.

A move toward stronger identity checks or heavier geofencing could leave the product intact while testing how much of the moat came from access rather than execution.

Regulatory language would carry the second major marker. Another FCA-style warning, a US agency statement, a derivatives venue action, or a court fight over a perps-like product would carry more weight than generic debate over whether the platform is decentralized enough.

The important marker is what regulators identify as the problem: the product, the users reached, the operator, the interface, or the lack of checks.

The onshore market is the third marker. If CME, Cboe, Kalshi-style venues, or other regulated platforms keep adding crypto exposure that feels closer to perpetual trading, Hyperliquid will be competing against better legal certainty on one side and looser access on the other.

That is a powerful position only if traders continue to value the access premium more than the regulatory discount.

CZ’s remarks put that tension in unusually plain language. Hyperliquid’s moat may be real precisely because Binance cannot copy it.

The unresolved risk is whether the same moat can survive the legal pressure that follows when on-chain perps become too important for regulators and regulated exchanges to ignore.

DeFi,Derivatives,Exchanges,Featured,Legal,Trading,Binance,Bitcoin,ethereum,Hyperliquid,regulationBinance,Bitcoin,ethereum,Hyperliquid,regulation#called #Hyperliquids #KYC #model #awesome1782273865

{kind=link}