On July 9, Phantom and the Hyperliquid Policy Center urged the CFTC to remove rules they say “unduly impede” fintech firms from working with registered derivatives markets.

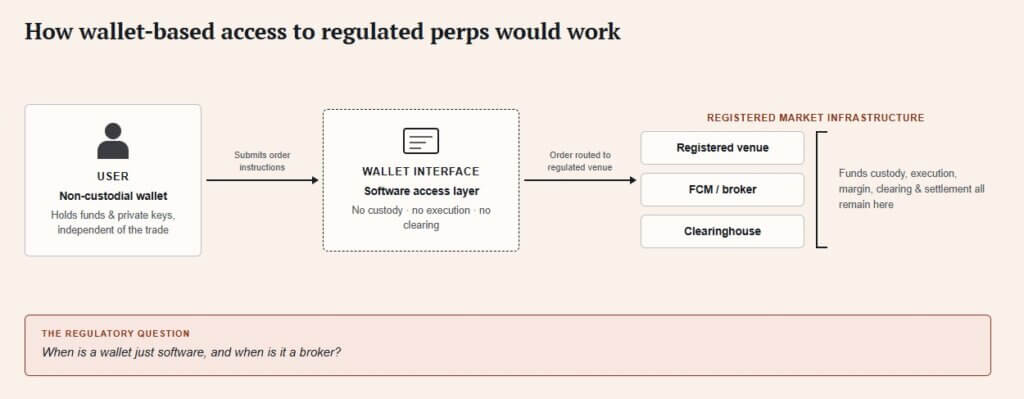

Phantom presents itself as the software in the middle, rather than the custodian. Users retain control of their funds and private keys, while trades are executed directly between them and registered venues.

Phantom already offers Hyperliquid through its interface, though US users still cannot access it.

American traders still need a regulated path to reach on-chain perpetual futures through a wallet, and this filing is Phantom’s attempt to build one.

Three specific requests

The letter asks the CFTC for three things: protocol developers should avoid triggering registration requirements simply for building on-chain software, registered exchanges and clearinghouses should get a clear path to perform functions like execution, margining, and recordkeeping on public blockchains, and non-custodial wallets should avoid classification as introducing brokers when they provide technical access to markets.

Phantom’s filing pushes that regulated perpetual futures and event contracts could eventually live in the same wallet app someone already uses to hold tokens.

On Mar. 17, the CFTC’s Market Participants Division issued Phantom no-action relief, meaning staff would not recommend enforcement if Phantom failed to register as an introducing broker for a specific kind of software access to registered futures commission merchants, introducing brokers, and designated contract markets.

Phantom only provides the interface. Users submit orders directly to registered firms, which hold the assets and control execution and routing.

The letter also attaches real conditions: conflict disclosures, risk disclosures, independent user access to the registered collaborator, and recordkeeping and marketing controls, plus joint liability arrangements with the collaborators Phantom connects with.

The relief applies to staff at the Market Participants Division and rests on the specific facts Phantom presented, falling short of a binding position for the full Commission.

The CFTC’s own letter states that different facts could void the position and that the division can modify, suspend, terminate, or restrict it at any time.

July’s filing asks the CFTC to develop a broader, codified version of the registered-market-access model logic for any wallet in Phantom’s position.

Wallet, broker, and clearinghouse

A futures broker traditionally sits between an investor and the market, with an introducing broker soliciting and accepting orders and futures commission merchants and clearinghouses handling customer funds, margin, and settlement.

The March relief describes Phantom’s role as front-end software that lets users route orders directly to registered entities, without Phantom touching funds, orders, or execution.

Whoever owns the interface decides which products appear first, how risk warnings get presented, how margin gets explained, and how a person moves from holding an asset to trading on margin against it.

| Function | Traditional derivatives model | Phantom’s proposed wallet-access model | Why it matters for investors |

|---|---|---|---|

| User interface | Broker or exchange account | Wallet app becomes the front-end screen | The trading experience may move into the app investors already use |

| Custody of assets | Broker, FCM, or exchange-linked structure | Registered collaborators hold or control regulated market assets | Wallet access does not necessarily mean the wallet holds margin funds |

| Order routing | Broker or platform routes orders | User submits orders directly to registered entities through software | Key line between “software interface” and “broker activity” |

| Execution | Registered exchange or venue | Registered venue | Regulated market infrastructure still matters |

| Margin and clearing | FCMs and clearinghouses | FCMs and clearinghouses, potentially with onchain components | The risk engine remains regulated, even if the interface changes |

| Risk disclosures | Broker/exchange onboarding | Wallet plus registered collaborators must present disclosures | Investors may encounter leverage warnings inside wallet UX |

| Accountability | Broker, venue, clearinghouse, user | Wallet, registered venue, clearing entity, user | Responsibility becomes harder to parse when the front end is separated from custody and execution |

The CFTC issued an advisory on May 29 covering 24/7 trading, clearing, and settlement, noting that blockchain networks, stablecoins, and smartphone-based apps are pushing more platforms toward always-on access.

The advisory also warned that continuous trading raises its own risks around liquidity, volatility, spreads, manipulation, and system reliability.

Coinbase and Kalshi introduced regulated perpetual crypto futures for US investors in May, the first time such products became available through domestic regulated exchanges, describing perps as no-expiration derivatives that can offer up to 50-to-1 margin.

The 2025 global perpetual futures volume was $61.7 trillion, so even 1% of that volume migrating into regulated US channels equals roughly $617 billion, and 5% amounts to over $3 trillion.

The risk that travels with the convenience

Wallet access eliminates a custody handoff: traders can keep tokens in their own wallets while using them in derivatives positions.

It also blurs the question: if a user gets liquidated, misreads a funding rate, or clicks through a risk disclosure without absorbing it, responsibility now has to sort itself out among the wallet, the registered venue, the clearing entity, and the user.

The CFTC’s own May advisory supplies the risk language for that, citing reduced liquidity, wider spreads, more manipulation risk, and operational and cybersecurity exposure that demands real-time surveillance at a level most consumer-facing apps are only beginning to build.

| Scenario | What happens | What investors see | Who gains power |

|---|---|---|---|

| Bull path: wallets become the front door | The CFTC codifies broader guidance for non-custodial interfaces and registered venues plug into wallet apps | Perps, event contracts, and tokenized derivatives appear inside familiar wallet interfaces | Wallets gain user ownership, distribution power, and transaction revenue |

| Middle path: limited access under strict conditions | Relief expands slowly but remains tied to registered collaborators, disclosures, recordkeeping, and marketing controls | Some regulated products appear in wallets, but onboarding still feels like a broker-style process | Wallets become distribution partners, while brokers and venues keep the legal relationship |

| Bear path: access stays narrow or case-by-case | The CFTC avoids broad codification, or courts/regulators tighten wallet-based derivatives access | US users stay in broker/exchange accounts for regulated products, while onchain perps remain offshore or geofenced | Futures brokers, centralized exchanges, and registered venues keep the front door |

Two ways this regulatory fight resolves

A bullish outcome would let more regulated venues connect directly with non-custodial wallets under broader CFTC guidance.

Perpetual futures, event contracts, and tokenized derivatives are starting to appear as ordinary in-wallet crypto products, with brokerage products fading from the user’s daily experience, and wallets are picking up pricing power, user ownership, and transaction revenue that offshore venues currently hold.

The bear case leaves wallet-based derivatives behind a regulatory gate. US users would still need broker or exchange accounts for regulated products, while on-chain perpetuals remain offshore or geofenced. Futures brokers and centralized exchanges keep control of access.

The outcome will shape where regulated crypto derivatives live: inside broker and exchange accounts, or in the wallet apps investors already use. The harder part is bringing that convenience to market without discarding protections that took decades to build.

Derivatives,Exchanges,Featured,Regulation,Wallets#Phantom #pulls #onchain #perps #wallet #war #ahead #July #deadline1783684680

{kind=link}