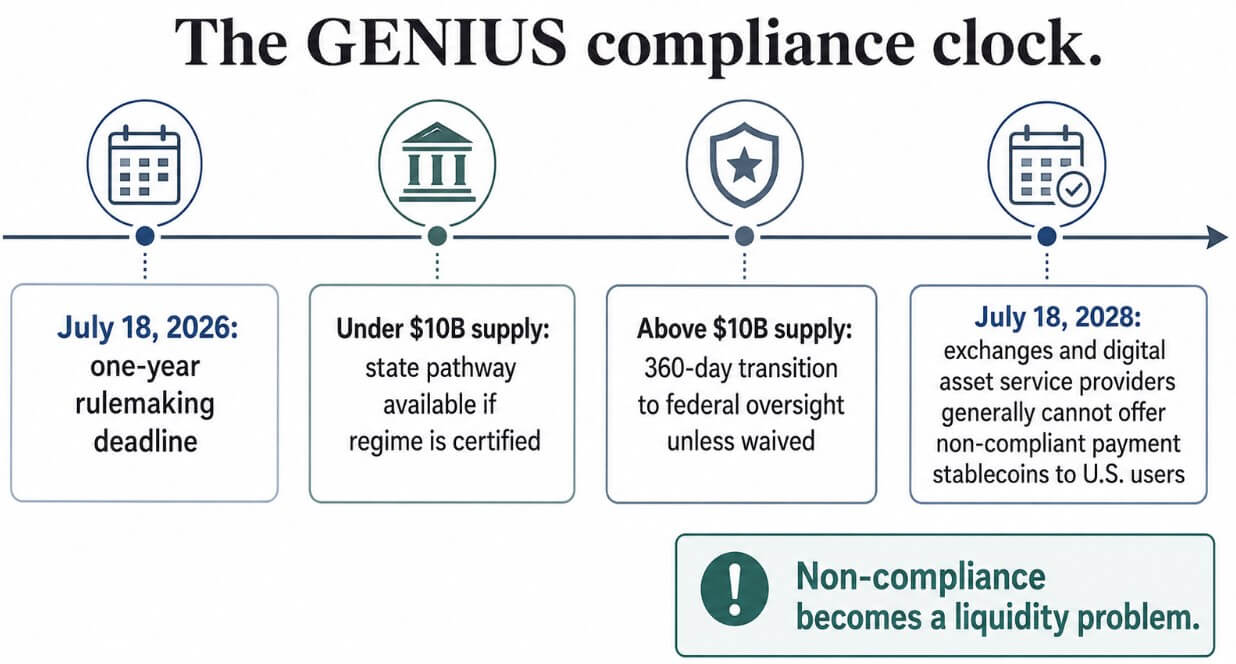

The GENIUS Act’s one-year rulemaking deadline lands on July 18, and markets have mostly priced it as a legitimacy milestone for stablecoins.

Mike McCluskey, CEO of tx, and Zaheer Ebtikar, chief strategy officer at Plasma, read it as a cost-visibility event that decides which issuers can afford to keep operating.

GENIUS became law on July 18, and Section 13 gives federal and state regulators 1 year to finalize the rules implementing it. That deadline triggers the full compliance stack under the law, including reserve composition, monthly audits, licensing, anti-money laundering programs, and redemption standards.

Ebtikar told CryptoSlate:

“The compliance burden is not a one-time licensing fee. It is a recurring operational infrastructure involving segregated reserve accounts, monthly independent audits, transaction monitoring, and dedicated compliance personnel.”

He added that mid-sized issuers face steep costs before issuing a single dollar at meaningful scale, and that dollar figure barely moves whether an issuer has $200 million or $2 billion in circulation.

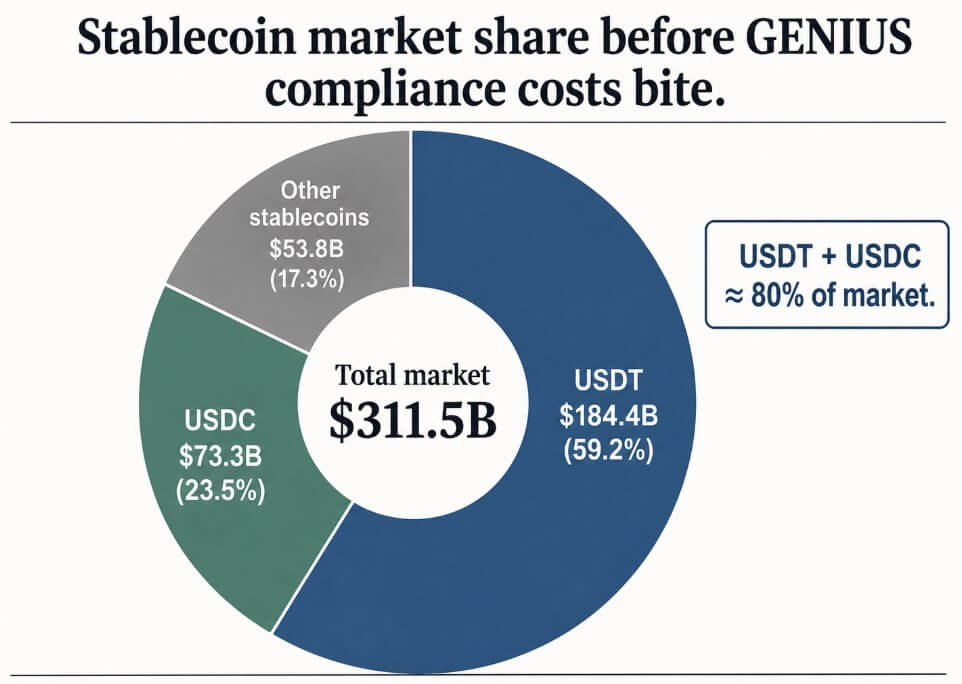

DeFiLlama puts the total stablecoin market cap at around $311.5 billion, and the two largest issuers, USDT at $184.4 billion and USDC at $73.3 billion, already control roughly 80% of it.

Circle’s own USDC page lists $73.7 billion in circulation as of June 29, and the company holds those reserves in cash and cash equivalents, mostly through the Circle Reserve Fund, an SEC-registered government money market fund managed by BlackRock.

Mike McCluskey explained the mechanism behind that concentration:

“The GENIUS Act doesn’t eliminate smaller participants through explicit prohibition, but by establishing a compliance cost floor that is inherently regressive.”

The fixed costs of legal review, reserve verification, AML systems, and licensing land on a mid-market issuer at roughly the same dollar amount as on a multibillion-dollar incumbent, which turns survival into a function of balance-sheet durability.

He points to Circle and to the payment networks behind Open USD as the kind of scale that absorbs the floor.

Visa, Mastercard, Coinbase, and over 140 other businesses are building Open USD together, a dollar stablecoin designed to share reserve earnings with participants once the management fee is removed.

McCluskey said:

“The stability projected for H2 is tangible, yet it represents the equilibrium of an oligopoly where only the most capitalized issuers remain.”

The reserve math

GENIUS requires reserves to be held in highly liquid, government-backed assets, such as demand deposits, short-dated Treasuries, overnight repos, and government money market funds.

A registered public accounting firm must examine reserve reports monthly, and CEOs and CFOs must personally certify the numbers.

The law also treats issuers as financial institutions under the Bank Secrecy Act, pulling in anti-money-laundering programs, transaction monitoring, sanctions screening, and customer due diligence.

On top of that, issuers can’t pay holders interest or yield solely for holding the token, which pushes the economic fight toward reserve income and distribution deals.

McCluskey framed the reserve rules as the single biggest swing factor in the implementation as a whole:

“The reserve rules are the definitive catalyst, overshadowing all other implementation variables.”

GENIUS requires hyper-liquid, short-duration holdings, which strip smaller participants of yield-based margins on their reserves, and the yield ban then routes float income toward whichever business owns the end-user distribution relationship.

Issuers without that distribution layer compete solely on operational efficiency, and McCluskey said that “to identify the eventual victors in this regulatory environment, one must simply track the destination of reserve-generated income.”

At 3.74%, the current secondary-market yield on 3-month Treasury bills, a $200 million stablecoin generates about $7.5 million in gross reserve income per year.

A mid-sized compliance stack, say $15 million a year for audits, legal, AML systems, and licensing, costs double that issuer’s entire gross income before a single dollar of operating margin.

The same $15 million bill against a $10 billion issuer’s roughly $374 million in gross reserve income comes to about 4% of revenue.

That’s Ebtikar’s point: the dollar cost barely moves between a $200 million issuer and a $2 billion one, but the share of revenue that dollar figure represents varies by orders of magnitude.

| Stablecoin supply | Gross reserve income at 3.74% | Assumed annual compliance cost | Compliance cost as % of gross reserve income | Market-structure read |

|---|---|---|---|---|

| $200M | $7.5M | $15M | ~201% | Compliance overwhelms reserve income |

| $2B | $74.8M | $15M | ~20% | Survivable, but margin-constraining |

| $10B | $374M | $15M | ~4% | Scale starts absorbing the burden |

| $50B | $1.87B | $15M | ~0.8% | Compliance becomes a moat |

GENIUS gives issuers with under $10 billion in outstanding stablecoins a path to state regulation, provided regulators certify that the state regime is substantially similar to the federal framework.

Ebtikar argued that there is a different function in that carve-out:

“The $10 billion threshold outlined by GENIUS is framed as a concession to smaller issuers, but it may function more like a growth ceiling.”

Cross that line and an issuer has 360 days to transition to federal oversight, unless it secures a waiver. The compliance bill jumps exactly when an issuer is proving its product works.

Scale cuts both ways

The bull case runs through the institutions GENIUS targets directly. McCluskey described the appeal directly: institutional capital “hasn’t been awaiting a technical breakthrough, but rather a robust compliance framework capable of withstanding rigorous internal scrutiny.”

A bank-issued token or one from Circle now carries a different risk profile than USDT did before the law, de-risking the treasury conversation for corporate finance teams that couldn’t touch stablecoins before.

Pair that with Open USD’s distribution network of 140-plus businesses, and the bull case looks like a market that tilts more toward institutional investors, with fewer issuers carrying far more of the volume.

The bear case turns on timing: a mid-tier issuer approaching the $10 billion mark hits the federal transition clock just as it’s proving the product works.

Ebtikar expects the squeeze to show up in margins and reserve management well before any acquisition closes. He said:

“For smaller issuers, the gap between what they earn on reserves and what they spend on audits and licensing is simply not viable without scale.”

Then the exchange clock adds a deadline to all of it, as on July 18, 2028, digital asset service providers generally can’t offer a payment stablecoin to US users unless it comes from a permitted or qualifying foreign issuer.

Ebtikar framed the sequence:

“Any token outside the permitted perimeter loses exchange access, loses liquidity, and loses users, in that order.”

He added that founders watching that clock against a deteriorating balance sheet will find the choice to sell or partner “considerably straightforward.”

GENIUS makes stablecoins safer to hold and easier for a bank or corporate treasury desk to justify.

That legitimacy carries a price: a market with fewer issuers, each one large enough to spread audits, licensing, and reserve management across billions in float. Reserve income at scale pays for a compliance stack that reserve income at $200 million cannot.

GENIUS turns stablecoin issuance from a crypto product into a regulated-scale business, and on July 18, issuers start finding out which side of that line they’re on.

Featured,Regulation,Stablecoins#GENIUS #stablecoins #legal #July #decides #stablecoins #stay #competitive1783071072

{kind=link}