Bitcoin is close to losing $58,000, and the test below that level is whether the buyer stack that defined the post-ETF bull case still holds.

Near $58,522 with an intraday low near $58,135, the market is asking whether anyone will buy in size at current prices, and the answer depends on two pillars of demand that have both weakened in recent weeks.

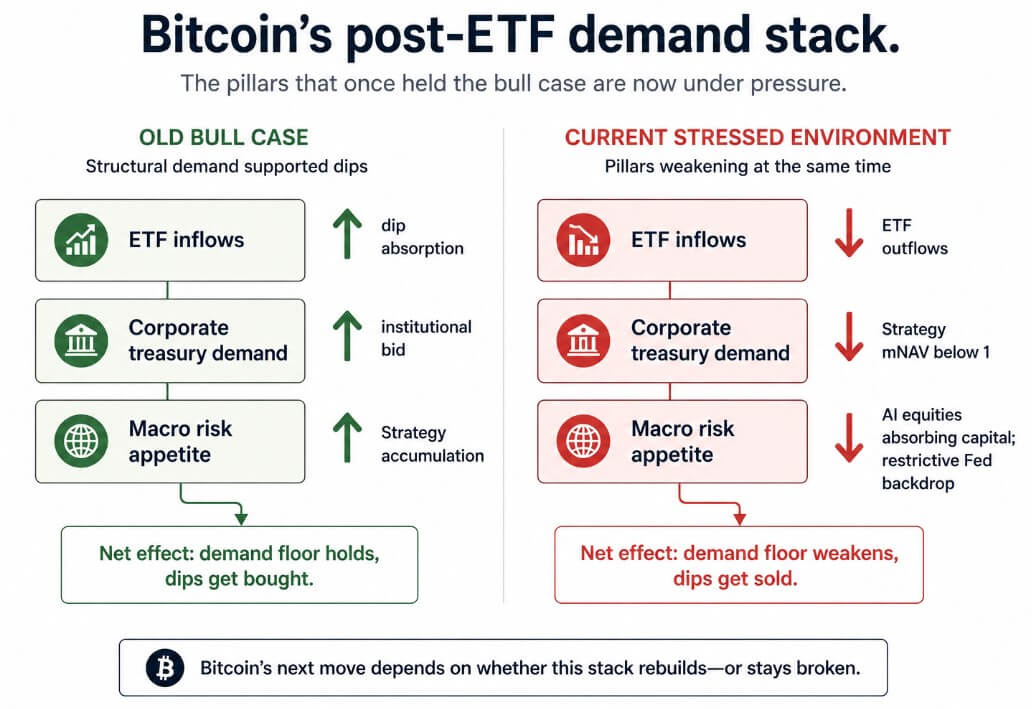

For most of the ETF era, bulls could point to a predictable answer. Regulated ETF wrappers created a repeatable demand channel, advisors and institutional allocators absorbed dips, and Strategy’s accumulation program turned every sell-off into a buying opportunity for the market’s largest corporate Bitcoin holder.

Each of those pillars is now weaker than it was six months ago, and the live test of $58,000 is the clearest evidence of that.

The old demand stack made dips feel investable, with bulls expecting the floor to catch any sell-off. Whenever Bitcoin pulled back, the narrative held that regulated products would bring in fresh capital, corporate treasuries were waiting to buy, and the ETF era had created a structural floor that was reliable regardless of flow cycles.

That argument survives only if the flows cooperate, and for roughly the past month, they have run in the opposite direction.

Where the buyer stack has broken down

Farside Investors’ data show US-traded spot Bitcoin ETFs have registered outflows for eight consecutive weeks, totaling nearly $2.2 billion in withdrawals.

CoinShares reported that digital asset investment products saw $1.67 billion in outflows for the week covered by its June 1 report, with Bitcoin alone accounting for $1.44 billion, the largest weekly Bitcoin outflow of 2026 at that point, while three-week cumulative outflows stood at $4.21 billion.

The ETF wrapper, which was supposed to bring a reliable institutional demand layer, has become the venue through which institutional capital is exiting.

Strategy’s enterprise value fell below the value of its Bitcoin holdings for the first time, with its mNAV at 0.99. The company authorized up to $1.25 billion in Bitcoin sales to build liquidity, marking its first actual Bitcoin sale since 2022.

Strategy had functioned as a narrative anchor: when the largest corporate holder was accumulating, dips felt like institutional confirmation, and the corporate treasury thesis reinforced every pullback as a buying opportunity.

With sales authorized and the mNAV below 1, that read has reversed, and the accumulation thesis is under its most direct test since the concept gained mainstream traction.

Reuters quoted a market participant noting that AI equities are absorbing risk capital that would previously have flowed into crypto, as Strategy’s situation raised doubts about corporate Bitcoin accumulation more broadly.

The Federal Reserve held rates at 3.5%-3.75% at its June 17 meeting, keeping the nominal-rate backdrop restrictive for non-yielding assets competing with equities that offer earnings growth, AI-sector momentum, and, in many cases, dividends.

US stock and bond markets close on July 3, while bond markets close early on July 2, compressing the ETF trading week precisely when the breakdown is live.

A break during thinner holiday liquidity would force crypto-native venues to absorb the initial move before ETF flows can validate or reject it upon Wall Street’s return.

| Demand pillar | Previous bull case | Current stress signal | Why it matters below $58K |

|---|---|---|---|

| Spot Bitcoin ETFs | Regulated wrappers would absorb dips through advisor and institutional demand | Eight weeks of outflows, totaling nearly $2.2B | The ETF channel becomes a source of supply instead of support |

| Strategy / treasury demand | Strategy accumulation made pullbacks feel investable | mNAV fell to 0.99; up to $1.25B in Bitcoin sales authorized | Corporate treasury demand is no longer treated as an automatic bid |

| Macro risk appetite | Risk-on capital could rotate into BTC | AI equities are absorbing capital that may have gone to crypto | Bitcoin competes with stronger equity narratives |

| Rates backdrop | Lower-rate expectations could support non-yielding assets | Fed held rates at 3.5%–3.75% | Cash and Treasuries remain competitive |

| Holiday-week liquidity | ETF sessions could help absorb selling | July 3 market closure compresses the trading week | Crypto-native venues may carry the first leg of a breakdown alone |

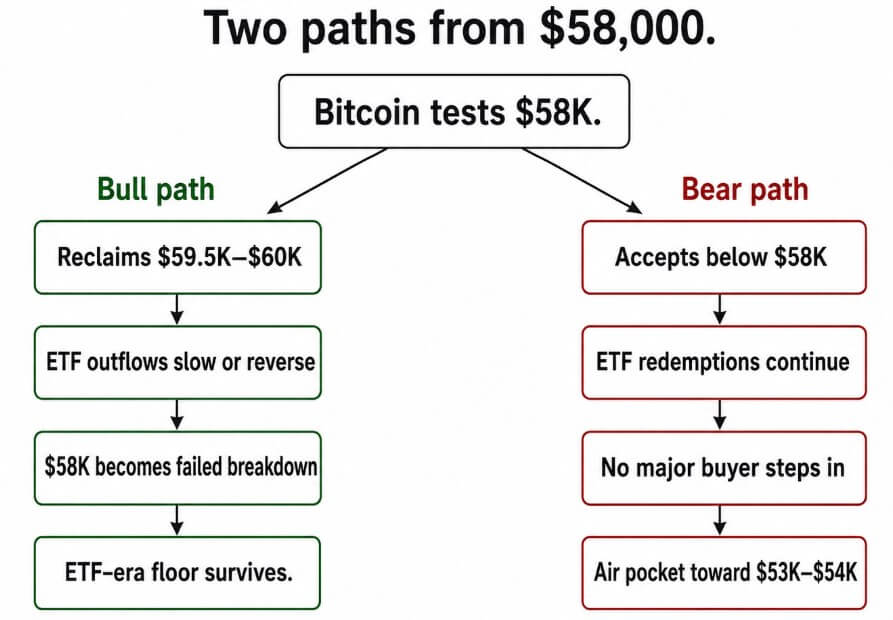

Two paths from $58,000

In the favorable outcome, Bitcoin quickly reclaims $59,500 to $60,000 once US markets reopen in full force. ETF outflows slow or reverse, spot demand appears during regular trading sessions, and $58,000 becomes a failed breakdown.

The demand stack looks damaged but functional, and the ETF-era floor survives its most direct test since regulated products launched.

For that to hold, the ETF bid would need to return in sufficient size to absorb the supply that drove prices down over the past month, and corporate treasury demand would need to re-emerge, with buying appetite replacing the authorized sales overhang.

In the less favorable outcome, Bitcoin accepts a close below $58,000 while ETF redemptions continue through the holiday week.

Recent commentary has placed $53,000 to $54,000 as the next serious downside zone, and the risk is that the move toward that level arrives as a slow air pocket, with orderly outflows and thin buyer participation.

Orderly selling into a buyer vacuum is slower to reverse and harder to read as a bottom in real time than a sharp liquidation event that exhausts itself quickly. A large institutional buyer or a sudden reversal in ETF flows could interrupt the move, but at current levels, both have been conspicuously absent.

Bitcoin can reach $53,000 on buyer withdrawals alone, with $58,000 failing while old dip-buyers hesitate. The ETF era created air pockets conditional on flows, and the flows are running in the wrong direction.

Analysis,Featured,Market,Price Watch#Bitcoin #fall #ETFera #floor #disappears1782905550

{kind=link}