Bitcoin’s more than $10 billion corporate credit market is still attracting new entrants after a June selloff triggered margin calls and drove its leading preferred shares far below par.

A new report from BitcoinTreasuries.net described the downturn as the sector’s first meaningful stress test, offering an early measure of whether companies can reliably build financing structures around their cryptocurrency reserves.

The selloff showed how quickly supposedly stable products can buckle when too much leverage piles in. Yet the market emerged bruised but operational. Dividend payments continued, secondary-market volumes reached record levels, and corporate treasuries kept adding Bitcoin to their balance sheets.

That resilience has drawn praise from industry proponents and sustained interest from prospective issuers, which are advancing plans for new yield-paying products across the US, Europe and Asia.

Investors are now betting that corporate Bitcoin holdings can support a wider market for preferred shares and similar debt-like products.

How leverage turned a stable trade into a cascade

Leverage piled into preferred shares that looked stable, then unwound in a rush of liquidations.

Strategy, the largest Bitcoin holding company with over 800,000 BTC, and Strive have used preferred shares to raise capital without relying entirely on common-stock sales or conventional debt. The securities typically carry a $100 stated value, pay fixed or variable dividends, and have no maturity date.

For issuers, the structure provides long-term capital that can be directed toward Bitcoin purchases or other corporate needs. Investors receive income above the yield available from many traditional fixed-income products without having to hold Bitcoin directly.

Strategy’s STRC and Strive’s SATA emerged as two of the largest instruments in the market. Strategy can adjust STRC’s dividend to keep the shares trading near $100, while SATA offers a variable payout and distributes dividends daily.

For months, both securities traded within relatively narrow ranges around par. That stability encouraged some investors to borrow money to increase their positions and amplify dividend income, BitcoinTreasuries.net said in its June corporate adoption report.

The strategy worked as long as the shares remained stable and the dividends exceeded the cost of financing the trade.

That calculation began to break down as Bitcoin fell below $60,000 in June and selling pressure spread across companies and securities tied to the cryptocurrency.

Beginning June 18, STRC and SATA moved sharply below par. Falling prices triggered margin calls for leveraged STRC holders, forcing them to sell into an already weakening market and driving further liquidations.

SATA also declined under pressure from its own market conditions and spillover from STRC’s selloff.

STRC eventually fell to about $75, roughly 25% below its stated value, while SATA declined to around $88. Bitcoin’s slide weighed on investor sentiment, even though preferred shares continued to pay their scheduled dividends.

Leverage turned products built for steady income into another source of volatility. Higher dividends might draw buyers after a selloff, but they offered little protection once indebted investors had to exit.

Raising the dividend also made the financing more expensive for the issuer. Strategy responded by increasing STRC’s annual payout to 12% and introducing a broader capital framework that included a $2.55 billion cash reserve, authority to repurchase preferred shares, and permission to sell some Bitcoin under specified conditions.

The company said the reserve was sufficient to cover about 17 months of expected preferred dividends and interest payments. It also acknowledged that STRC could remain substantially below its target range, leaving the market to determine whether the higher payout would be enough to restore demand.

Prices rebound as Bitcoin buying continues

Despite the June sell-off, the market stabilized faster than initial liquidations suggested, with prices rebounding, trading volumes hitting record highs, and corporate treasuries continuing to buy Bitcoin.

As of publication, STRC had recovered to about $87 from a low near $75, while SATA had climbed back to roughly $97.

The uneven rebound suggested investors were distinguishing between the two securities rather than abandoning the broader market.

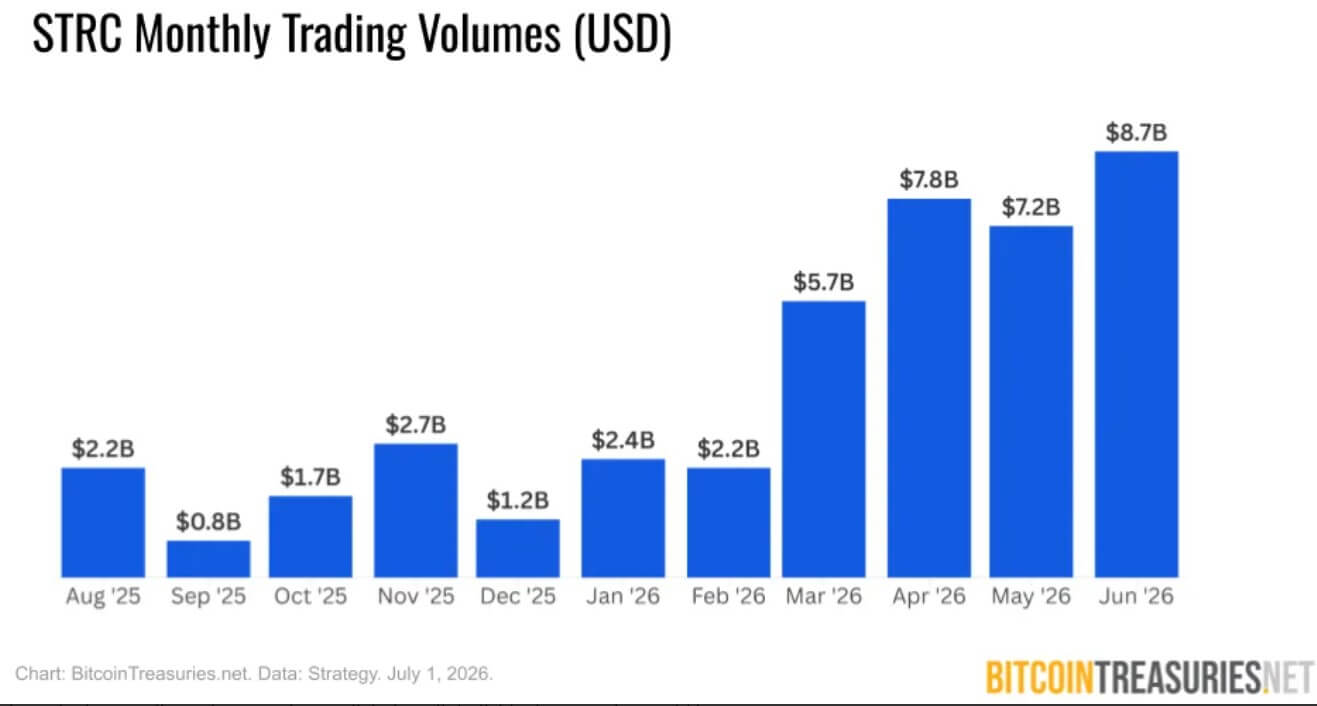

Trading activity also accelerated during the turmoil. Combined June volume for STRC and SATA exceeded $10 billion, even as both products traded below their $100 stated values.

STRC accounted for $8.7 billion of that total, its highest monthly volume on record, and posted two of its five busiest trading weeks. SATA generated nearly $1.5 billion, almost twice its May volume, with three of its four strongest weeks occurring during the month.

Trading held up through the sharp repricing. Buyers absorbed shares from leveraged sellers, keeping the market open and dividend payments uninterrupted.

However, the heavy secondary-market activity did not translate into fresh capital for the issuers. Neither STRC nor SATA was able to raise funds through at-the-market sales in June, as most transactions involved existing shares changing hands between investors.

Still, Strategy and Strive expanded their Bitcoin holdings despite the pause in preferred-share issuance.

Strategy added a net of 3,625 Bitcoin during the month, while Strive acquired 3,364 Bitcoin. Each spent about $200 million, leaving the two companies responsible for most of June’s corporate Bitcoin purchases.

Supporters saw the continued buying as evidence that June’s turmoil stemmed from excessive leverage in the securities, rather than fading confidence in corporate Bitcoin accumulation.

New entrants push the model beyond the US

The recovery in trading and continued corporate Bitcoin buying are now encouraging treasury companies to explore whether the credit model can expand beyond the US.

On July 10, Metaplanet provided the latest sign by announcing a joint study on tokenized credit instruments in Japan.

The Tokyo-listed company will work with Siiibo Securities, the yen stablecoin issuer JPYC, and the regulated security-token platform Progmat to examine products that use Bitcoin as a backing asset or as a source of credit support. Metaplanet recently acquired Siiibo for $13 million.

According to the firm:

“Digital credit backed by Bitcoin could evolve into instruments traded and settled globally on a 24/7/365 basis, with interest and distributions accruing on a daily prorated basis according to the holding period.”

The initiative targets longstanding barriers in Japan’s corporate credit market, where smaller and growing companies can face high costs for product design, distribution, investor administration, interest payments and redemptions.

Metaplanet and its partners said digital infrastructure could reduce some of those costs. Their proposal combines stablecoins for payments and distributions, security tokens for recording ownership and transfer rights, and Bitcoin as an asset supporting the securities.

The structure could calculate interest based on how long an investor holds a product, reducing reliance on conventional record dates. It could also allow trading and settlement outside regular market hours.

The project remains at an early stage, with no issuance date, return, distribution plan, or final structure in place. The companies have yet to decide whether to run a proof of concept.

Metaplanet has also not specified whether investors would have a direct legal claim to the designated Bitcoin. That detail will determine whether the products function as formally secured instruments or rely more broadly on the issuer’s balance sheet and cryptocurrency reserves.

Metaplanet holds 43,000 Bitcoin, ranking third among publicly traded companies by BTC holdings.

Bitcoin digital credit growth forecasts meet a more demanding market

Metaplanet’s planned entry adds weight to expectations that Bitcoin-backed credit will expand, though June’s selloff has given investors a clearer view of the risks behind those forecasts.

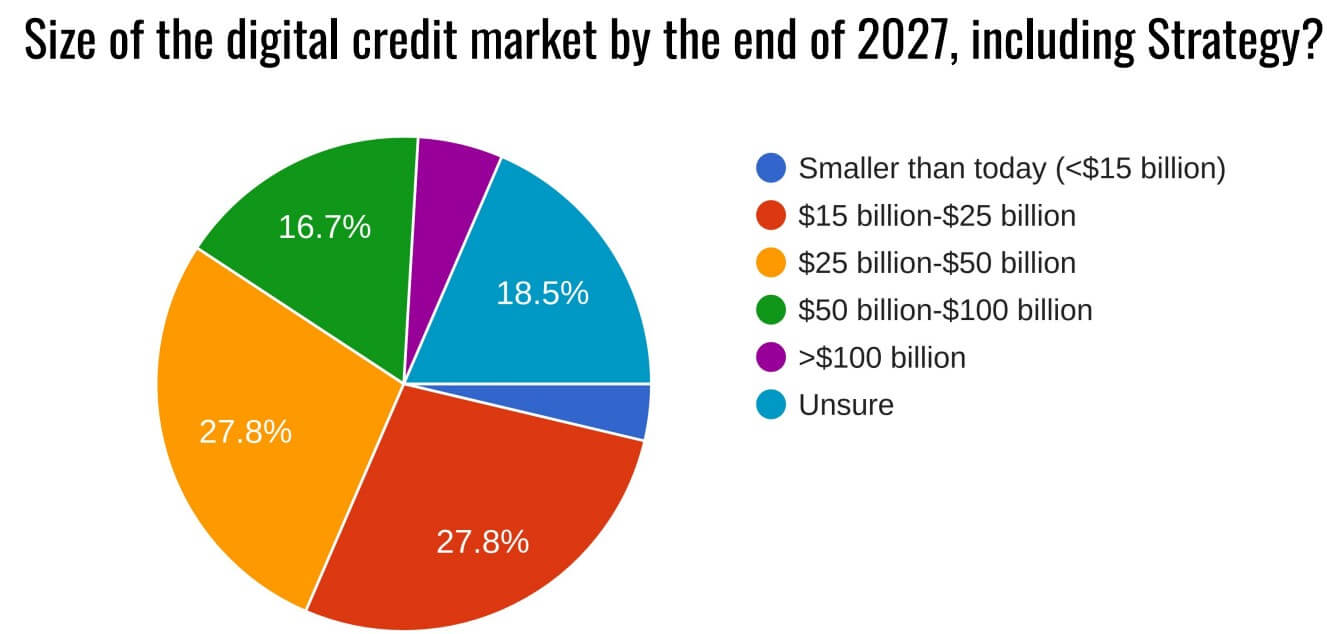

A BitcoinTreasuries.net survey found that 78% of respondents expect the digital credit market to grow through the end of 2027. Another 22% projected that outstanding supply could exceed $50 billion, with some expecting it to surpass $100 billion.

The results, however, reflect a group already predisposed to support the products. The report found that 87% of respondents viewed digital credit favorably and 72% had invested in the sector. About 76% also expected similarly sharp price declines to occur again.

That mix of confidence and caution offers a more measured assessment of June. Investors remain optimistic about the market’s long-term potential, even as they acknowledge that leverage and liquidity can drive large departures from par.

Michael Saylor has argued that Bitcoin makes digital credit easier to assess because its primary market risk is tied to a globally traded and continuously observable asset. Investors can track Bitcoin’s price and volatility in real time and incorporate those movements into their valuation models.

June proved Bitcoin-backed credit could survive a liquidation shock. Its next hurdle is persuading investors to fund new issuance after watching leading products trade below par.

Analysis,Digital Asset Treasuries,Featured,Market,Trading,Bitcoin,Metaplanet,SATA,Saylor,STRCBitcoin,Metaplanet,SATA,Saylor,STRC#Bitcoins #billion #credit #market #growing #major #selloff1783710234

{kind=link}