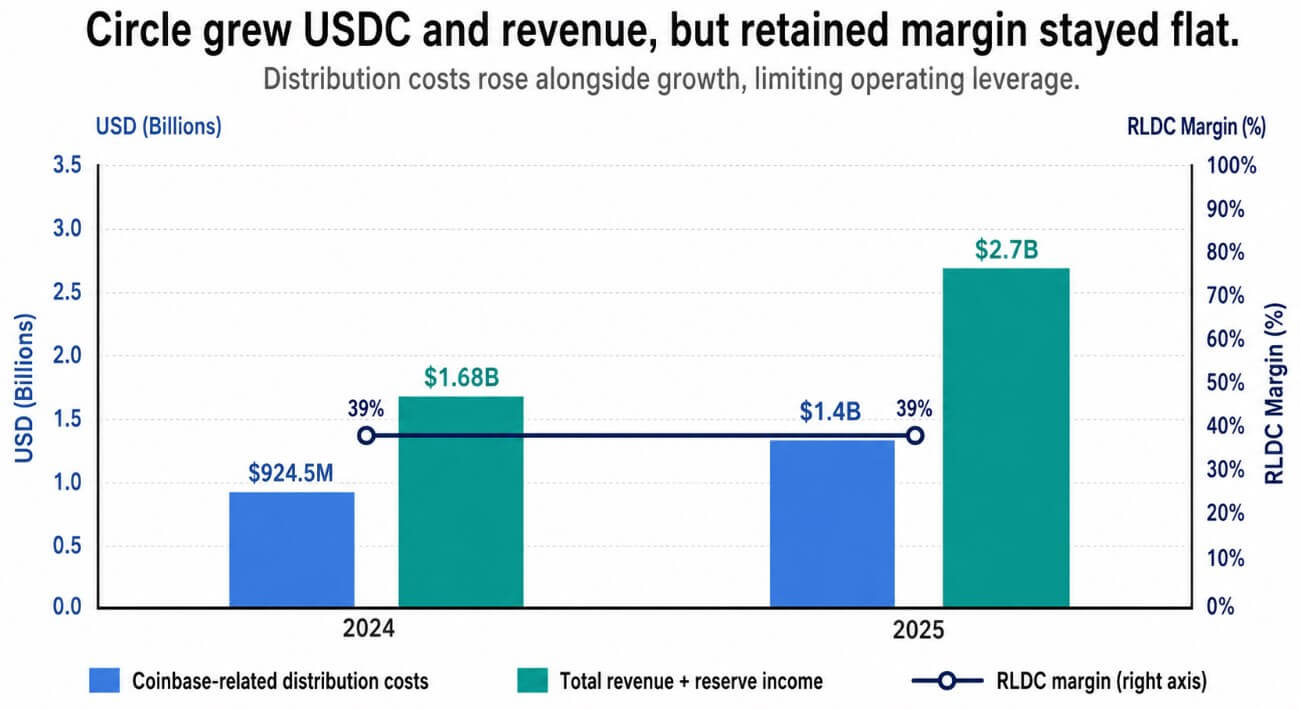

Circle incurred $1.4 billion in distribution costs connected to Coinbase in 2025, up from $924.5 million the year before, according to the company’s own 10-K filing.

Those distribution costs equaled roughly 51% of its total 2025 revenue and reserve income.

USDC circulation grew 72% year over year to $75.3 billion in the fourth quarter, and full-year revenue and reserve income climbed 64% to $2.7 billion. Circle retained a 39% margin after distribution and transaction costs, unchanged from 2024 even as growth accelerated.

Distribution and transaction costs consumed roughly 63% of Circle’s fourth-quarter reserve income. The pressure now extends beyond the Coinbase agreement, as alternative stablecoin models and trading venues seek a larger share of the reserve income generated by the USDC they distribute.

Circle and Coinbase entered into their current collaboration agreement in August 2023, with an initial three-year term that ends in August 2026.

The filing said Circle and Coinbase will discuss in good faith whether modifications are warranted before the initial term expires. If they do not agree to changes, the agreement automatically renews for another three years, provided both sides continue meeting their obligations.

Coinbase remains USDC’s largest centralized distribution partner and is also a participant in Open USD, a rival stablecoin model built by a consortium that includes Visa, Mastercard, and more than 140 other businesses.

Open USD shares reserve earnings with consortium members after deducting a management fee, giving Coinbase another benchmark for how stablecoin economics can be divided among distribution partners.

Where Hyperliquid fits in

Hyperliquid supplies the decentralized version of the same squeeze. USDH, launched by Native Markets as Hyperliquid’s native stablecoin, failed to displace USDC’s liquidity advantage.

Coinbase has said USDC stays the leading stablecoin on Hyperliquid, with roughly $5 billion in circulation there, and DeFiLlama puts USDC’s dominance of Hyperliquid’s stablecoin base near 97%.

USDC’s dominance didn’t stop Hyperliquid from extracting a price for it, as the protocol’s AQAv2 framework now directs roughly 90% of cost-adjusted reserve-yield revenue tied to aligned stablecoin supply back to Hyperliquid itself.

Assuming the entire $6.16 billion stablecoin base qualifies as aligned supply and earns a 3.5% reserve yield, it would generate about $215.6 million in annual gross reserve income. A simple 90% calculation produces roughly $194 million, though the framework’s cost adjustments mean the actual amount would differ.

JPMorgan has now flagged the Hyperliquid structure as a near-term earnings headwind for both Circle and Coinbase and a longer-term threat to Circle’s USDC economics.

The bank describes a setup in which both companies have reason to keep defending USDC’s distribution, with competition for that distribution eroding what each retains.

| Pressure point | What it controls | Economic leverage | Why it matters for Circle |

|---|---|---|---|

| Coinbase | Centralized USDC distribution | $1.4B in 2025 Coinbase-linked distribution costs | Circle depends on Coinbase for scale, but that access is expensive |

| Open USD | Alternative partner-sharing model | Reserve earnings shared with consortium members after a management fee | Gives distributors a benchmark for demanding more economics |

| Hyperliquid | Decentralized trading liquidity | AQAv2 routes roughly 90% of cost-adjusted reserve-yield economics to the protocol. | Shows a venue can keep USDC dominant while still extracting yield economics |

| August 2026 milestone | Circle-Coinbase agreement reset point | Automatic renewal possible, but modifications can be discussed | Creates a natural leverage checkpoint for both sides |

What Circle still has going for it

A platform can point to Open USD’s revenue-sharing terms as its bargaining chip with Circle, all without giving up USDC on its rails.

Hyperliquid has taken a similar approach by preserving USDC’s liquidity dominance while securing a larger share of the economics generated on its platform.

Circle’s sensitivity analysis, which holds USDC circulation and reserve allocation constant, estimates that a 100-basis-point rate increase would add $756 million to reserve income and $369 million to distribution and transaction costs. That would leave Circle with roughly $387 million, or 51%, of the incremental income after those costs.

Circle recently received final OCC approval to establish a national trust bank, a regulatory credential that competitors lacking a federal charter struggle to match.

If Open USD adoption stays slow, the Coinbase relationship renews on comparable terms, and Hyperliquid remains an isolated case, those conditions would support Circle’s ability to preserve its current margin and make its regulatory position the larger competitive advantage.

If other major exchanges, wallets, and DeFi protocols start asking for Hyperliquid-style or Open USD-style terms, and Coinbase enters its August 2026 discussions pointing to real alternatives, Circle’s retained share of reserve income has room to fall below its current level.

The scenarios below apply a 90% share to gross reserve income for illustration. AQAv2 payments are calculated based on cost-adjusted yield, so the actual amounts would differ.

| Stablecoin base affected | Reserve yield | Gross annual reserve income | 90% distributor/protocol share |

|---|---|---|---|

| $6.16B | 3.5% | $215.6M | $194.0M |

| $10B | 3.5% | $350.0M | $315.0M |

| $25B | 3.5% | $875.0M | $787.5M |

| $50B | 3.5% | $1.75B | $1.58B |

USDC can keep expanding under that path, with each additional dollar of circulation becoming less valuable to the company that issues it.

The stablecoin competition investors have watched for years assumed that the winner would be whoever commanded the largest supply.

Circle’s 2025 numbers point elsewhere, as USDC can keep winning that count, with the platforms holding its users deciding how much of the profit behind that count belongs to Circle.

Analysis,Featured,Stablecoins#USDCs #surge #exposed #expensive #truth #Circles #stablecoin #dominance1784113627

{kind=link}