A group of crypto tokens tied to some of the industry’s largest revenue-generating applications could be positioned for a revaluation as Congress moves closer to establishing a federal rulebook for digital-asset markets.

The Digital Asset Market Clarity Act, known as the CLARITY Act, would define regulatory responsibilities for crypto assets and the companies that trade them. Supporters say the legislation could give banks, asset managers, and other traditional financial firms greater confidence to conduct business on public blockchains.

Asset management firm Grayscale expects that shift to favor applications already processing transactions and collecting fees, particularly those built around trading, lending, and other financial services.

The potential catalyst comes after a prolonged market downturn left many of their tokens valued at relatively low multiples of the revenue their protocols generated over the past year.

The Senate Banking Committee advanced the legislation in May after the House approved an earlier version in 2025. Grayscale said the bill could progress as soon as next month, though its timing and final provisions remain subject to negotiations in Congress.

Trading tokens lead the potential winners

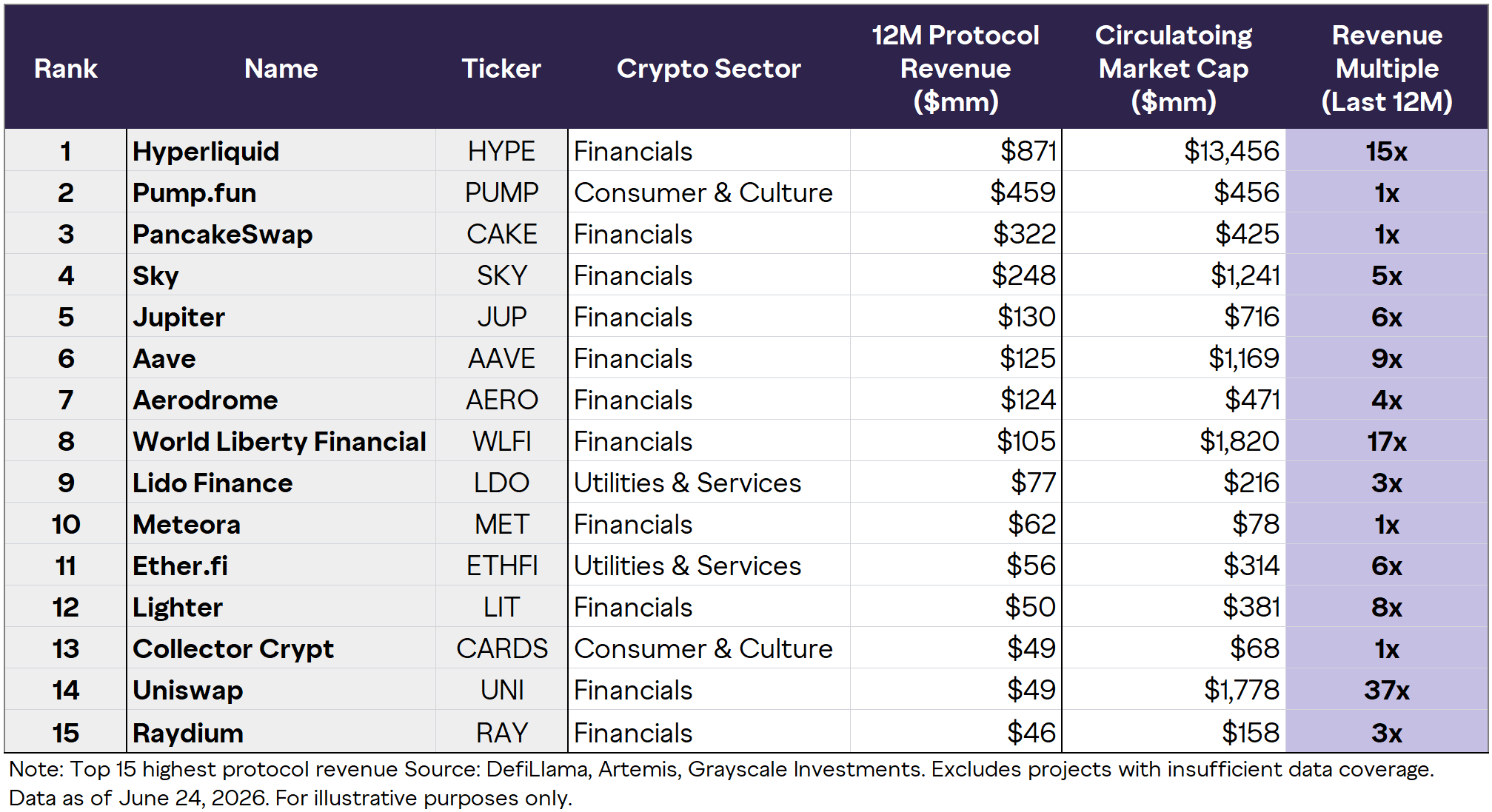

Hyperliquid sits at the front of the group because of the scale of its derivatives business.

The decentralized trading platform generated $871 million in protocol revenue over the 12 months through June 24, more than any other application in a ranking compiled by Grayscale.

HYPE, its native token, carried a circulating market capitalization of approximately $13.46 billion, giving it a trailing revenue multiple of about 15. That valuation is higher than that of most tokens on the list, but Hyperliquid also generated almost twice as much revenue as its closest competitor.

Clearer US market-structure rules could expand the pool of assets and participants entering blockchain-based trading venues. Greater certainty over whether digital assets fall under securities or commodities regulation could also make it easier for regulated institutions to connect with on-chain markets.

The opportunity extends across decentralized exchanges and trading aggregators.

PancakeSwap generated $322 million over the trailing 12 months, while its CAKE token had a circulating value of $425 million. That placed it near 1 times protocol revenue, among the lowest multiples in the ranking.

Jupiter, a Solana-based trading aggregator, recorded $130 million of revenue and a $716 million circulating market capitalization, equivalent to about 6 times revenue. Aerodrome generated $124 million in revenue and traded at nearly 4 times revenue, while Meteora generated $62 million in revenue and carried a valuation of only $78 million.

Raydium’s $46 million in revenue compared with a $158 million circulating market value, leaving the Solana exchange token at roughly 3 times revenue.

Those platforms could benefit if the legislation encourages issuers to bring more regulated assets onto blockchains. Each new tokenized security, commodity, or fund would need markets where investors can buy, sell, and provide liquidity.

Uniswap offers a different valuation profile. The decentralized exchange generated $49 million in protocol revenue, but its UNI token carried a circulating market value of about $1.78 billion, equal to 37 times revenue and the highest multiple among the 15 protocols.

That premium suggests investors already assign substantial value to Uniswap’s brand, market position, and prospects for future fee generation.

It also means the token may have less room for a valuation-driven rebound than competitors trading at lower multiples, unless regulatory clarity produces a significant increase in activity or strengthens the connection between protocol fees and UNI holders.

Pump.fun, the Solana-based memcoin launchpad, ranked second overall with $459 million in annual protocol revenue and a circulating market capitalization of $456 million.

While the Solana-based platform is less directly tied to institutional finance, clearer rules around digital-asset issuance and trading could still affect its business.

Its approximately 1-times revenue multiple reflects both the scale of its fee generation and investor doubts about whether activity associated with speculative token launches can remain durable through changing market cycles.

Aave and Sky could gain from tokenized credit

Lending protocols may benefit from the next stage of on-chain adoption as tokenized assets move beyond trading and become collateral for loans.

Aave generated $125 million in trailing protocol revenue. Its AAVE token had a circulating market capitalization of approximately $1.17 billion, placing its multiple near 9.

The protocol allows users to borrow and lend digital assets through automated markets. An increase in regulated stablecoins, tokenized funds, and blockchain-based securities could broaden the pool of assets available as collateral and attract more borrowers and lenders to its markets.

Institutional participation could be particularly significant. Banks and asset managers entering public blockchains would require credit markets, collateral-management systems, and sources of liquidity alongside trading venues.

Aave already operates much of that infrastructure, though the extent of its benefits would depend on whether institutions use open protocols directly or favor permissioned systems and regulated intermediaries.

Sky, the project previously known as Maker, could also gain from the expansion of tokenized credit and stablecoins.

The protocol generated $248 million over the past year, the fourth-highest total in the ranking. Its SKY token had a circulating market capitalization of about $1.24 billion, equivalent to 5 times the protocol’s revenue.

Sky’s exposure to stablecoins and tokenized real-world assets gives it a direct link to the type of financial activity that Grayscale expects the legislation to encourage. Greater use of blockchain-based Treasury products, credit instruments, and cash-like tokens could increase demand for the infrastructure used to issue, borrow, and settle those assets.

President Donald Trump-backed World Liberty Financial also appears among the largest revenue producers, with $105 million over 12 months. Its WLFI token was valued at approximately $1.82 billion, or 17 times revenue.

That relatively high multiple indicates that investors are assigning value beyond the protocol’s current fee generation. Its political connections and evolving product strategy may also make direct comparisons with more established lending and exchange protocols difficult.

Staking and infrastructure may benefit indirectly

An increase in on-chain financial activity would also create demand for the systems that secure blockchain networks and allow investors to earn returns from their assets.

Lido Finance generated $77 million in trailing protocol revenue, while its LDO token had a circulating value of $216 million. Its 3-times revenue multiple places it among the cheapest assets in the group on that measure.

Lido provides liquid staking services, allowing users to commit assets to help secure blockchain networks while receiving tokens that can continue to circulate through decentralized finance applications.

Ether.fi operates in a related part of the market. The protocol generated $56 million over the period and carried a circulating market value of $314 million, giving its ETHFI token a multiple of about 6.

If the CLARITY Act encourages more assets and transactions to move onto public networks, staking providers could benefit from higher demand for blockchain security and yield-bearing products. Growth in tokenized finance could also create more uses for liquid staking tokens as collateral across trading and lending applications.

The effect would probably arrive less directly than it would for exchanges or lending markets. Staking remains subject to separate legal questions, while the final legislation may not resolve every issue surrounding the treatment of staking services or rewards.

Still, the inclusion of Lido and Ether.fi among the industry’s largest revenue generators shows that the economic activity behind crypto extends beyond trading. Financial applications depend on underlying networks, validators, and liquidity systems that may also expand as transaction volumes rise.

Low Multiples Leave Room for a Repricing

The broader investment case rests on how little the market currently pays for the revenue generated by many of these applications.

Twelve of the 15 protocols in Grayscale’s ranking traded at single-digit multiples of trailing revenue. Pump.fun, PancakeSwap, Meteora, and Collector Crypt were each valued at approximately 1 times revenue. Lido and Raydium traded at nearly 3x, while Aerodrome was valued at 4x.

Sky, Jupiter, and Ether.fi carried multiples between 5 and 6. Lighter, an on-chain trading platform that generated $50 million in revenue, traded at around 8x, while Aave stood at 9x.

Grayscale argues that the valuations look even lower when viewed against potential earnings or cash flow because many blockchain applications operate without the large staffing, property, and administrative expenses associated with traditional companies.

The comparison has limits. Protocol revenue does not always belong to token holders in the same way corporate revenue belongs to a company and ultimately supports its shareholders.

Fees can flow to validators, liquidity providers, developers, protocol treasuries, or users. Some applications also distribute tokens to attract activity, creating an economic cost that may not appear in headline revenue figures.

Circulating market capitalization can further understate a project’s eventual valuation when a large portion of its token supply remains locked and scheduled for future release.

For investors, the strongest potential winners will therefore be protocols that combine revenue growth with a clear mechanism for directing economic value toward their tokens. Those links can include fee distributions, token repurchases, staking demand, or governance rights over protocol income.

The CLARITY Act would not guarantee higher prices for any of the assets. It could, however, reduce a regulatory discount that has limited institutional participation and complicated how investors value US-facing crypto projects.

Featured,Legislation,Market,Tokenization,Trading,CLARITY Act,Grayscale,HyperliquidCLARITY Act,Grayscale,Hyperliquid#crypto #tokens #biggest #winners #CLARITY #Act1782479266

{kind=link}